Lab on Applied VAR Modelling

Pedro J. Perez

2020, April

- Objective

- Gali (1999) model:

- Data preparation

- Model Specification

- Estimation of the VAR

- Validation of the VAR

- Data preparation

- VAR in reduced form (uses):

- Granger causality

- Forecasting

- Granger causality

- VMA representation

- Obtaining the VMA with R

- Obtaining the VMA with R

- Uses of VAR: “structural” analysis:

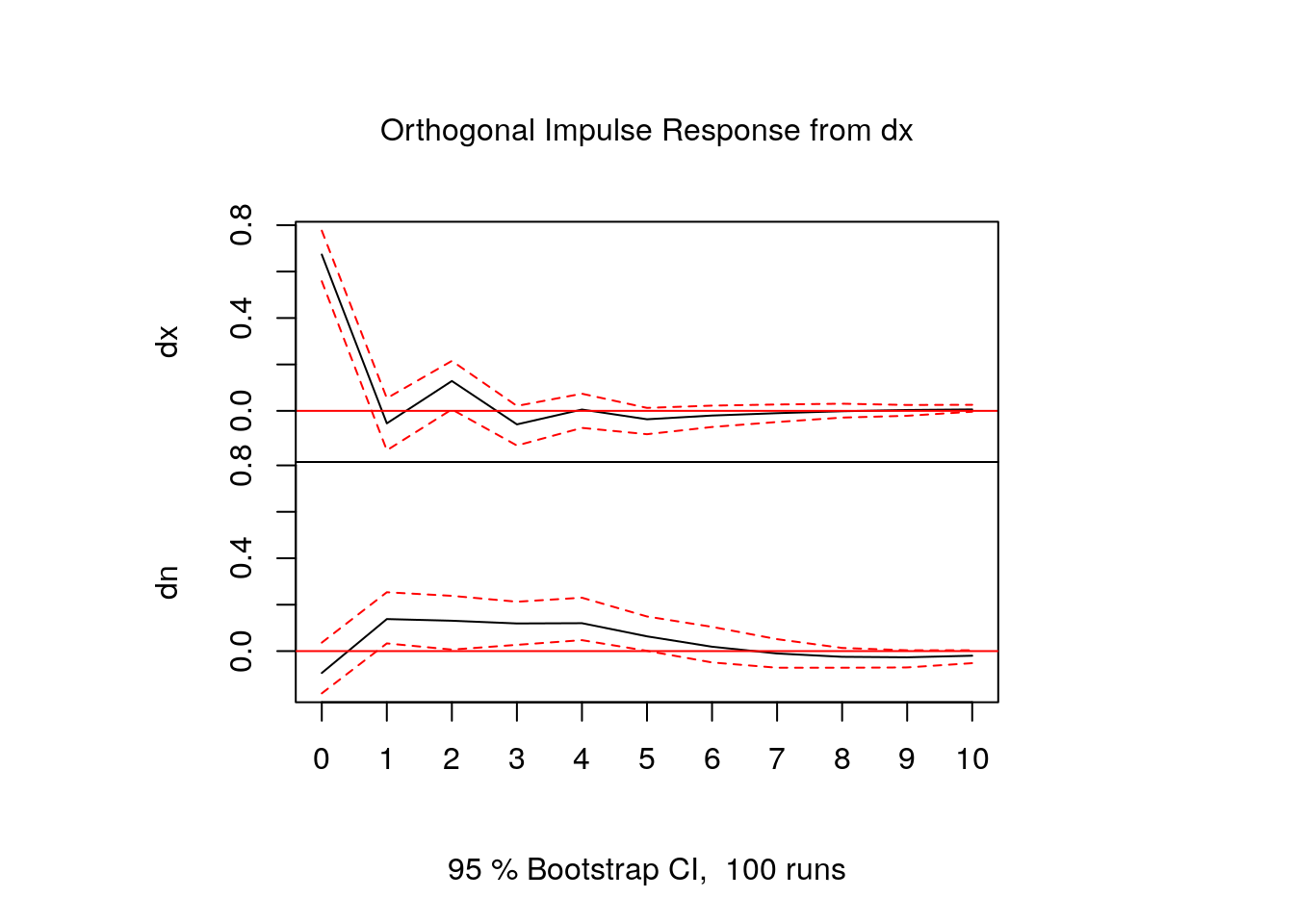

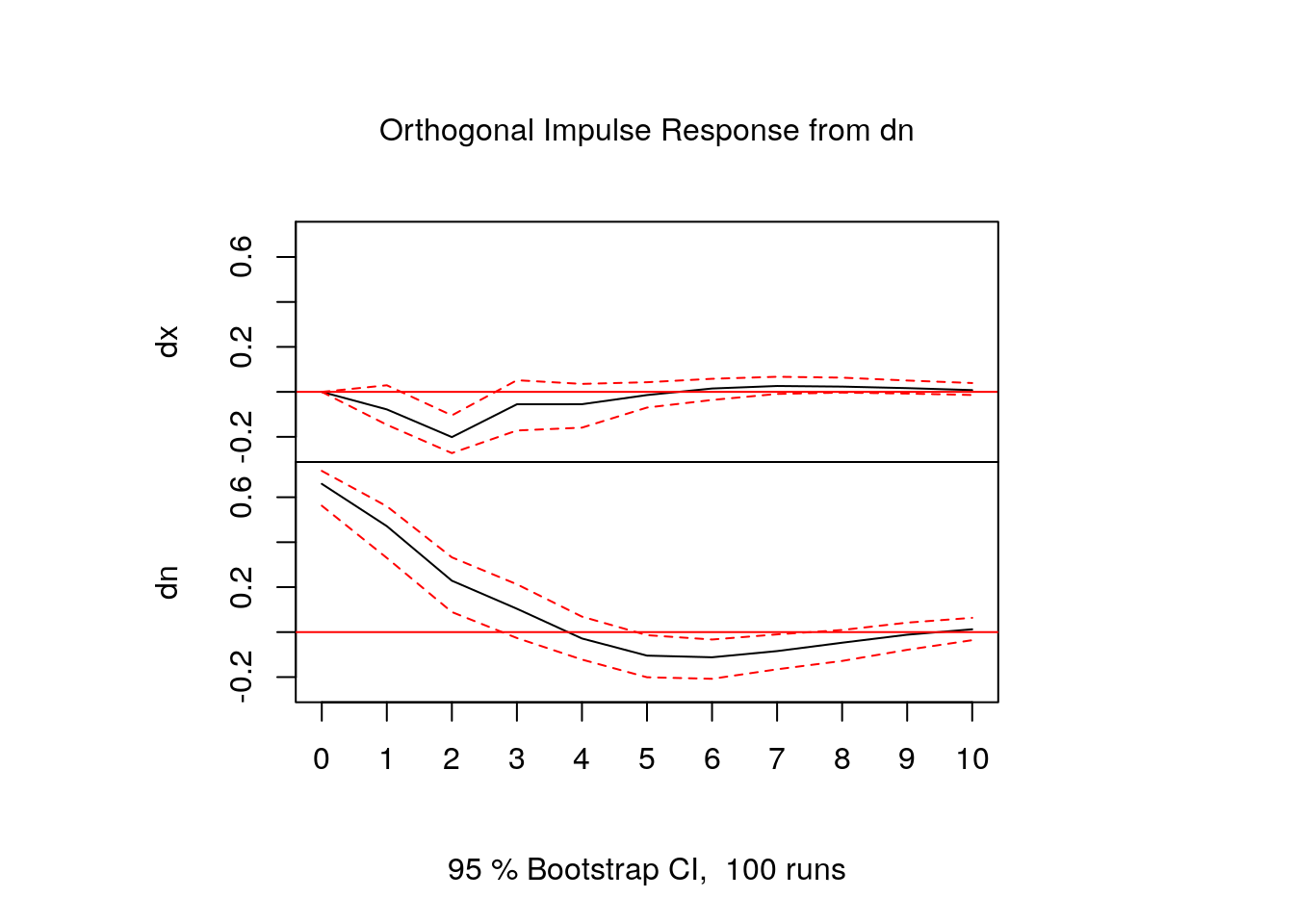

- IRFs

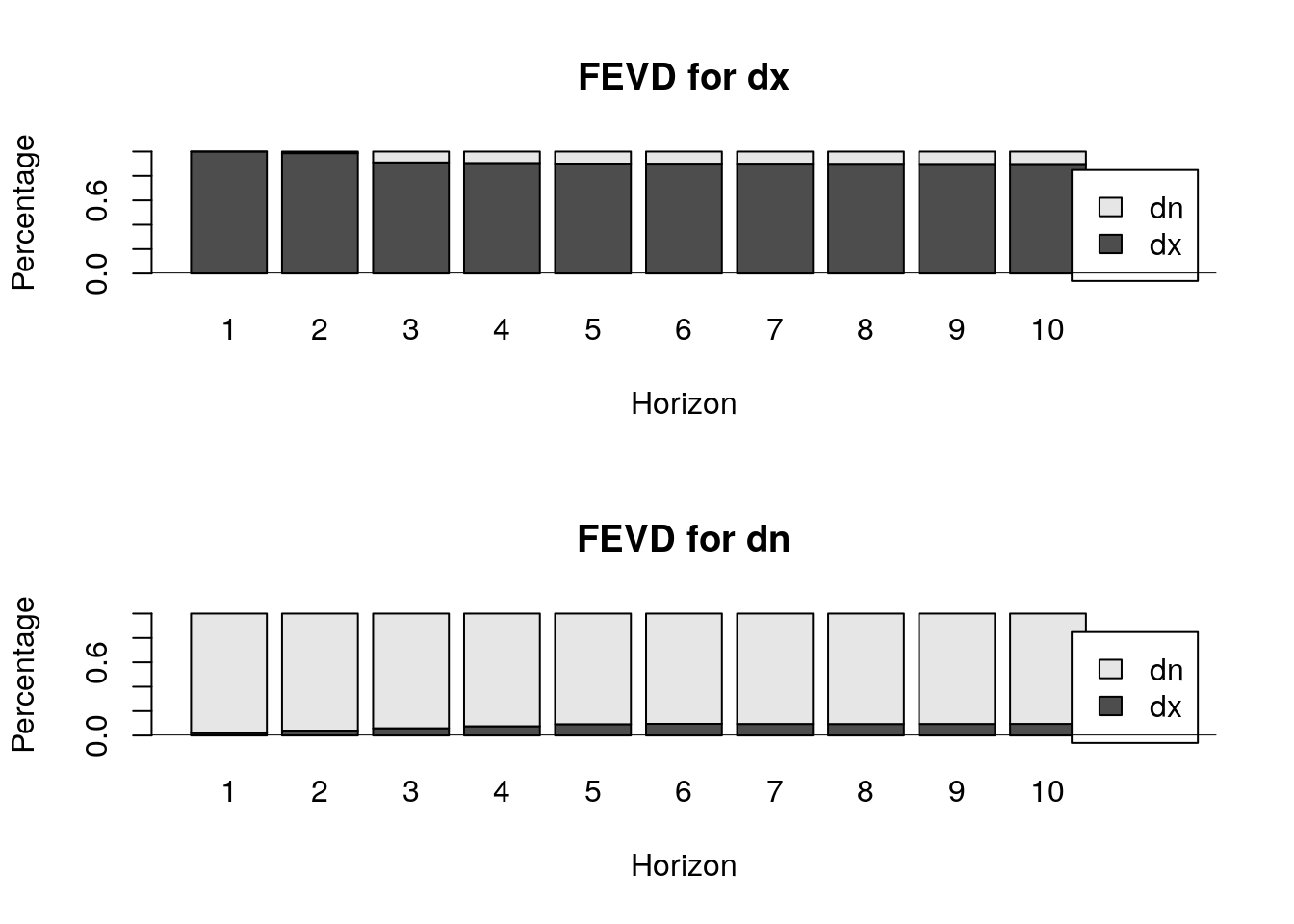

- FEVD

- IRFs

1. Objective

Lab to illustrate the possibilities of VAR modelling with R

We are going to use the R package

varswritten by Bernhard Pfaff. A short description of the functionalities of the Pfaff’s package could be found here. For a more detailed exposition, please go hereTo illustrate the different topics in VAR modelling, we are going to use as an example the analysis and data used in Gali (1999) paper : "Technology, Employment, and the Business Cycle: Do Technology Shocks Explain Aggregate Fluctuations?

2. Gali (1999) model

In his paper, Gali estimates a bivariate VAR with productivity and hours to look mainly at the response of hours to a technology shock

In fact we are going to “replicate” the Gali paper but only his benchmark model:

U.S. quarterly data for 1948:1 - 1994:4 from Citibase

bivariate VAR model: productivity(\(x_{t}\)) and hours(\(n_{t}\))

\(y_{t~}=~\left[ x_{t~},n_{t}\right] ^{^{\prime }}\), both variables in (log) first differences

To replicate in your PC the Gali analysis, copy and paste the following R script:

- Be aware that you have to change the path to load the data. The

DATA_gali_99.csvfile with the data are in Aula virtual

#- 1) dowload the DATA_gali_99.csv in you PC

gali_data <- read.csv("./datos/DATA_gali_99.csv", sep = ";", header = T) #- change the path to the file

#- 2) defining the ts variables

GDP <- ts(gali_data$GDPQ, start = c(1947, 1), end = c(1994, 4), frequency = 4)

Hours <- ts(gali_data$LPMHU, start = c(1947, 1), end = c(1994, 4), frequency = 4)

Productivity <- GDP/Hours

#- 3) setting the sample

GDP <- window(GDP, start = c(1948, 1), end = c(1994, 4))

Hours <- window(Hours, start = c(1948, 1), end = c(1994, 4))

Productivity <- window(Productivity, start = c(1948, 1), end = c(1994, 4))

#- 4) Taking log's and indexing (1948:1 = 100) the variables

lGDP <- 100 + 100 * log(GDP/GDP[1])

lHours <- 100 + 100 * log(Hours/Hours[1])

lProductivity <- 100 + 100 * log(Productivity/Productivity[1])

#- 5) Taking first differences of the log-variables

dy <- diff(lGDP, lag = 1, difference = 1)

dn <- diff(lHours, lag = 1, difference = 1)

dx <- diff(lProductivity, lag = 1, difference = 1)

#- 6) Install & loading the vars package

install.packages("vars")

library(vars)

#- 7) Creating a matrix with the two series

variables <- cbind(dx, dn)

#- 8) Estimating the VAR

VAR(variables, p = 4, type = "const")Data preparation

Step by step the analysis will be:

- Let’s start opening R and loading the Gali(99) data. The original data can be found at the Estima web page (on the file galiaer1999.zip)

#----loading data(csv format with (;) for separator and with labels or header)

gali_data <- read.csv(here::here("datos", "DATA_gali_99.csv"), sep = ";", header = TRUE)- Let’s see what variables are inside the data file

#-- str() displays the internal structure of an R object

str(gali_data[, 1:8]) #-- only for the 1:8 columns of gali_data'data.frame': 192 obs. of 8 variables:

$ GDPQ : num 1240 1247 1255 1270 1284 ...

$ LHEM : num NA NA NA NA 57976 ...

$ LPMHU: num 91.7 91.4 91.6 92.9 93.3 ...

$ P16 : num 101203 101662 102060 102386 102691 ...

$ FM2 : num NA NA NA NA NA NA NA NA NA NA ...

$ FYGM3: num 0.38 0.38 0.737 0.907 0.99 ...

$ PUNEW: num 21.7 22 22.5 23.1 23.6 ...

$ CANN : num NA NA NA NA NA NA NA NA NA NA ...The data are quarterly and runs from 1947:1 to 1994:4

The

varspackage only works with data in a specific format: time series or ts. To convert our data in the time series format we are going to use thets()function in RGDPQ is the measure of aggregate output

LPMHU is labor input (hours)

#-- creating the time series with ts(): GDP, Hours & Productivity (labor productivity)

GDP <- ts(gali_data$GDPQ, start = c(1947, 1), end = c(1994, 4), frequency = 4)

Hours <- ts(gali_data$LPMHU, start = c(1947, 1), end = c(1994, 4), frequency = 4)

Productivity <- GDP/Hours- We will start the analysis with the sample 1948:1 to 1994:4

#-- Changing the start date of the series to 1948:1

GDP <- window(GDP, start = c(1948, 1), end = c(1994, 4))

Hours <- window(Hours, start = c(1948, 1), end = c(1994, 4))

Productivity <- window(Productivity, start = c(1948, 1), end = c(1994, 4))#-- Taking log's and indexing (1948:1 = 100) the variables

lGDP <- 100 + 100 * log(GDP/GDP[1])

lHours <- 100 + 100 * log(Hours/Hours[1])

lProductivity <- 100 + 100 * log(Productivity/Productivity[1])#-- Taking first differences of the log-variables

dy <- diff(lGDP, lag = 1, difference = 1)

dn <- diff(lHours, lag = 1, difference = 1)

dx <- diff(lProductivity, lag = 1, difference = 1)Finally, the two variables used in the Gali’s VAR were dx and dy: first difference of productivity and hours (both in logs) [growth rate’s of labor productivity (dx) and hours (dn)]

That is, Hours and Productivity are supposed to be I(1) variables. Obviously, Gali checked this before

The VAR is estimated using data from 1948:1 - 1994:4 for the variables dx dn

- To estimate the VAR models we are going to use the R vars package, let’s load the vars package

#-- You will have first to install the vars packages with: install.packages('vars')

library(vars)

variables <- cbind(dx, dn) #-- Creating a matrix with the two seriesWe are now ready to estimate the VAR model: the vars package has a function, the VAR() function, that estimate VAR models by OLS

Simply writing in the R console the following:

VAR(variables, p = 4, type = "const"), we will estimate a VAR model for the 2 variables in the matrix called “variables” with a constant and 4 lags(p), … but, why 4 lags?

- How p should be fixed? How to select the order of the VAR model?

Model Specification

We have already decided which variables to include in our VAR model, the sample, if the variables are I(1) vs. I(0) , and the deterministic components . In this case we have almost finished the model specification. Almost, because … we need to decide the order of the VAR.

How to select (p) the order of the VAR?

For a more detailed exposition go to Lütkepohl(2011), pp. 10-11

The idea is that we have to select an order(p) sufficiently large to ensure that the residuals shown no autocorrelation but without exhausting the degrees of freedom.

The order of the VAR could be selected by:

Sequential testing procedures

Model selection criteria

The package “vars” has the

VARselect()function that allows to apply easily the 2nd approach to select p.Remember that for viewing the syntax and options of an R function you could use the R

args()functionIf you need additional explanations you should call the R-help typing at the R console the following:

?VARselect

function (y, lag.max = 10, type = c("const", "trend", "both",

"none"), season = NULL, exogen = NULL)

NULLvariables <- cbind(dx, dn) #-- Creating a matrix with the two series

VARselect(variables, lag.max = 8, type = "const")$selection

AIC(n) HQ(n) SC(n) FPE(n)

2 2 1 2

$criteria

1 2 3 4 5 6

AIC(n) -1.5849704 -1.6556248 -1.6258129 -1.6125929 -1.612723 -1.6200352

HQ(n) -1.5416478 -1.5834204 -1.5247267 -1.4826249 -1.453873 -1.4323036

SC(n) -1.4781307 -1.4775586 -1.3765202 -1.2920736 -1.220977 -1.1570629

FPE(n) 0.2049551 0.1909782 0.1967674 0.1994038 0.199406 0.1979932

7 8

AIC(n) -1.6087278 -1.5938218

HQ(n) -1.3921144 -1.3483267

SC(n) -1.0745290 -0.9883966

FPE(n) 0.2002998 0.2033812- Three criteria (AIC,HQ &FPE) choose p=2; BUT, as our data are quarterly, probably, as Gali does, a more sensible choice would be p=4

Finally, we are now ready to estimate our VAR with p=4. Let’s go!!!

Estimation of the VAR

- Estimating the VAR model (in reduced form)

#- we are saving the estimation results in the object 'our_var'

our_var <- VAR(variables, p = 4, type = "const")- Let’s see the estimation results. The best way is through the function

summary()

VAR Estimation Results:

=========================

Endogenous variables: dx, dn

Deterministic variables: const

Sample size: 183

Log Likelihood: -361.495

Roots of the characteristic polynomial:

0.7609 0.7609 0.4955 0.4955 0.4125 0.3886 0.3886 0.04377

Call:

VAR(y = variables, p = 4, type = "const")

Estimation results for equation dx:

===================================

dx = dx.l1 + dn.l1 + dx.l2 + dn.l2 + dx.l3 + dn.l3 + dx.l4 + dn.l4 + const

Estimate Std. Error t value Pr(>|t|)

dx.l1 -0.096398 0.076313 -1.263 0.2082

dn.l1 -0.118188 0.075043 -1.575 0.1171

dx.l2 0.175137 0.078470 2.232 0.0269 *

dn.l2 -0.231832 0.092432 -2.508 0.0131 *

dx.l3 0.032485 0.076911 0.422 0.6733

dn.l3 0.114524 0.092560 1.237 0.2176

dx.l4 0.009445 0.076295 0.124 0.9016

dn.l4 -0.016682 0.076980 -0.217 0.8287

const 0.389255 0.083809 4.645 6.7e-06 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.6734 on 174 degrees of freedom

Multiple R-Squared: 0.1575, Adjusted R-squared: 0.1187

F-statistic: 4.065 on 8 and 174 DF, p-value: 0.0001858

Estimation results for equation dn:

===================================

dn = dx.l1 + dn.l1 + dx.l2 + dn.l2 + dx.l3 + dn.l3 + dx.l4 + dn.l4 + const

Estimate Std. Error t value Pr(>|t|)

dx.l1 0.30492 0.07547 4.040 8e-05 ***

dn.l1 0.71481 0.07422 9.631 <2e-16 ***

dx.l2 0.05422 0.07761 0.699 0.4857

dn.l2 -0.12814 0.09142 -1.402 0.1628

dx.l3 0.02442 0.07607 0.321 0.7485

dn.l3 0.10069 0.09154 1.100 0.2729

dx.l4 0.05498 0.07546 0.729 0.4672

dn.l4 -0.13815 0.07613 -1.815 0.0713 .

const 0.07376 0.08289 0.890 0.3748

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.666 on 174 degrees of freedom

Multiple R-Squared: 0.4759, Adjusted R-squared: 0.4518

F-statistic: 19.75 on 8 and 174 DF, p-value: < 2.2e-16

Covariance matrix of residuals:

dx dn

dx 0.45344 -0.06341

dn -0.06341 0.44351

Correlation matrix of residuals:

dx dn

dx 1.0000 -0.1414

dn -0.1414 1.0000- Let’s see the (same) estimation results, but in other format: the \(A_{i}\) matrices

[[1]]

dx.l1 dn.l1

dx -0.09639832 -0.1181884

dn 0.30492251 0.7148050

[[2]]

dx.l2 dn.l2

dx 0.1751366 -0.2318322

dn 0.0542222 -0.1281375

[[3]]

dx.l3 dn.l3

dx 0.03248468 0.1145240

dn 0.02442320 0.1006887

[[4]]

dx.l4 dn.l4

dx 0.009444778 -0.01668181

dn 0.054984423 -0.13815029- After estimation and before to use or transform our VAR we have to check their validity, mainly looking at the residuals

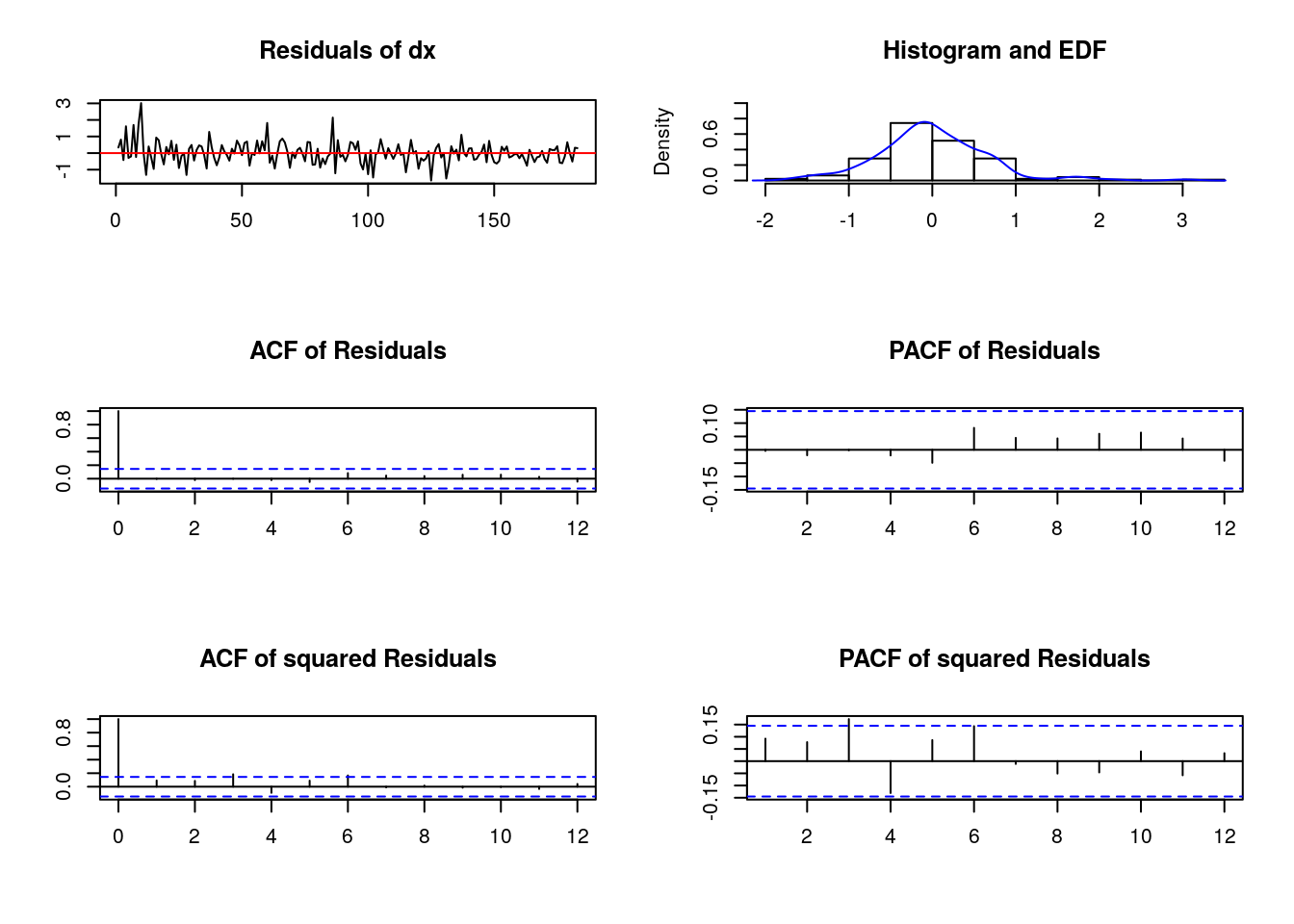

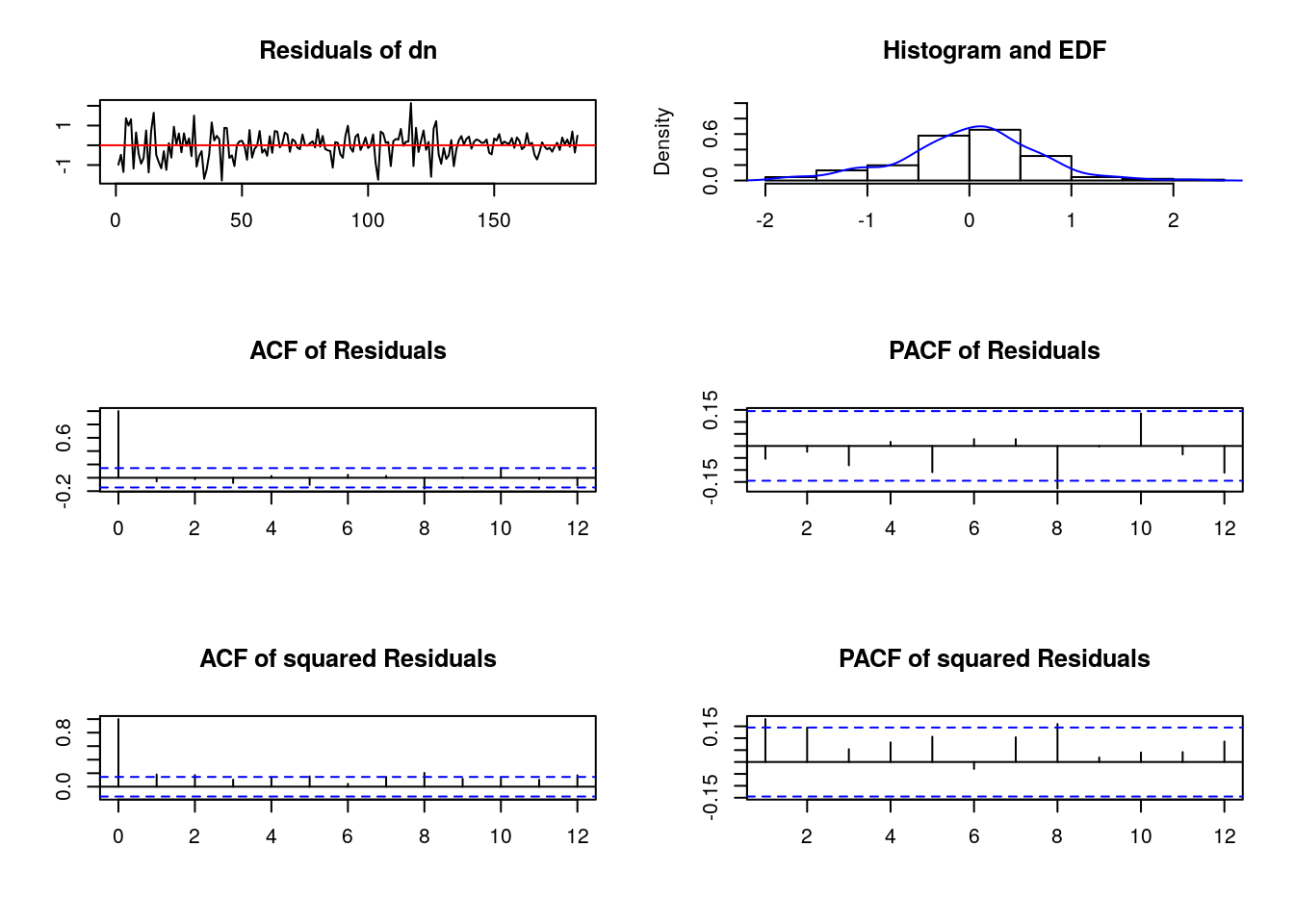

Validation of the VAR

- Stability and roots

#- Checking stability(eigenvalues of the companion coefficient matrix must have modulus less than 1)

roots(our_var, modulus = TRUE) #-- Returns a vector with the eigenvalues[1] 0.76092599 0.76092599 0.49550808 0.49550808 0.41252822 0.38858444 0.38858444

[8] 0.04376503- Accessing the Y-fitted, with the fitted() function

#-- We can access fitted-Y with fitted()

print(fitted(our_var)[1:4, ]) #---- Y-fitted fot the first 4 observations dx dn

1 1.0117163 -0.6248601

2 1.0254013 -0.5451213

3 0.7838393 0.1710223

4 0.9547305 -0.2437604- Accessing the residuals

#-- We can access the residuals with residuals()

print(residuals(our_var)[1:4, ]) #-- print the four first residuals dx dn

1 0.3374632 -0.9774587

2 0.8121841 -0.4816300

3 -0.4217890 -1.3515856

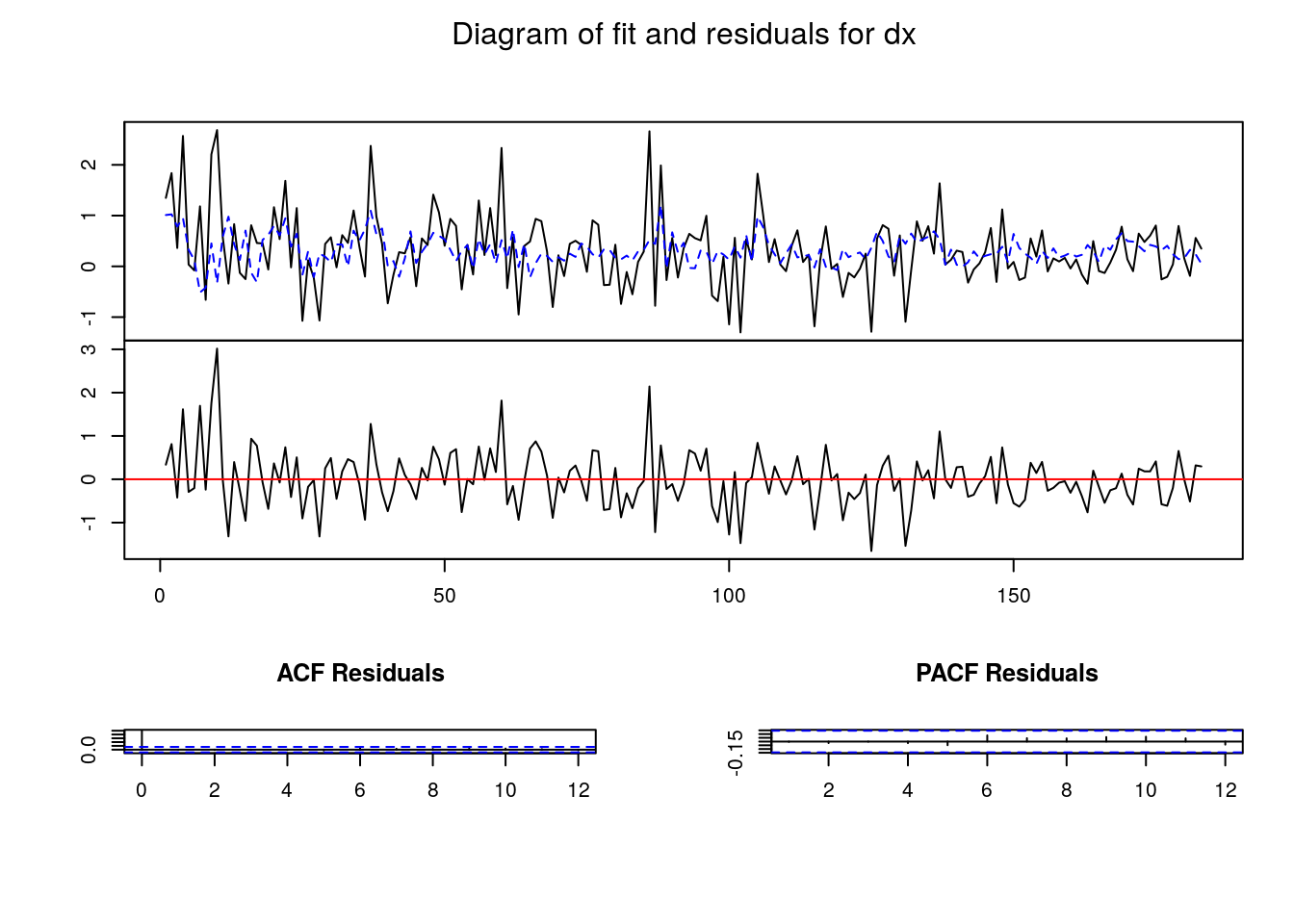

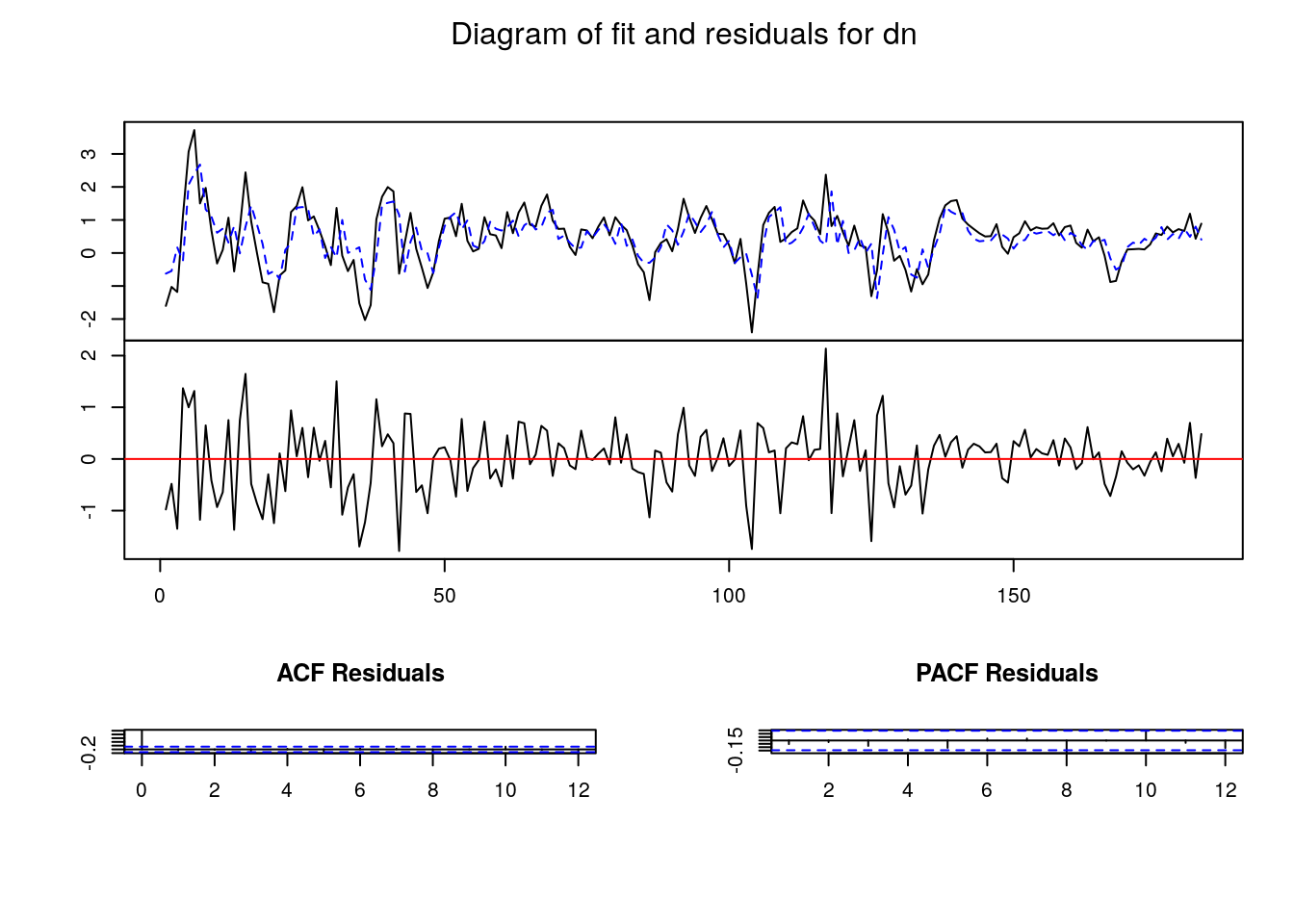

4 1.6152363 1.3684236- “Plotting” our VAR

- Testing on the residuals

#-- We can test autocorrelation and normality of residuals

serial.test(our_var, lags.pt = 8) #-- 8 lags for autocorrelation portmanteau test

Portmanteau Test (asymptotic)

data: Residuals of VAR object our_var

Chi-squared = 24.955, df = 16, p-value = 0.07061$dx

JB-Test (univariate)

data: Residual of dx equation

Chi-squared = 68.644, df = 2, p-value = 1.221e-15

$dn

JB-Test (univariate)

data: Residual of dn equation

Chi-squared = 3.6281, df = 2, p-value = 0.163

$JB

JB-Test (multivariate)

data: Residuals of VAR object our_var

Chi-squared = 75.873, df = 4, p-value = 1.332e-15

$Skewness

Skewness only (multivariate)

data: Residuals of VAR object our_var

Chi-squared = 16.763, df = 2, p-value = 0.000229

$Kurtosis

Kurtosis only (multivariate)

data: Residuals of VAR object our_var

Chi-squared = 59.109, df = 2, p-value = 1.461e-13- “Plotting” our “residuals test”

#-- There is a function plot or method associated to the autocorrelation test

our_serial <- serial.test(our_var, lags.pt = 8) #-saving our autocorr.test in object 'our_serial'

plot(our_serial)

3. VAR in reduced form (Uses)

The two principal uses of VAR models in reduced form are testing (causality testing) and forecasting, BUT the most used instruments in the VAR methodology are IRF & FEVD.

IRF & FEVD only have a clear meaning if we transform our reduced form VAR model to an structural VAR. We will develop this idea in a while

Testing in a VAR

After validation, the VAR could be used for testing, for example, for testing Granger causality

As we said, if the residuals are normally distributed (Gaussian) like (\(v_{t}\rightarrow N(0,\Sigma _{v})\)) the OLS estimator has desirable asymptotic properties. In particular, it will be asymptotically normally distributed, and then, if the VAR is stable, usual inference procedures are asymptotically valid: t-statistics could be used for inference about individual parameters and F-test for testing hypothesis for sets of parameters.

Granger causality

Granger causality: Granger called a variable X causal for Y if the information in past and present values of X is helpful for improving the forecast of Y. If Granger causality holds, this does not guarantee that X causes Y. But, it suggests that X might be causing Y.

In the context of VAR models, if we want to test for Granger-causality, we need to test zero constraints in some of the coefficients.

Sometimes econometricians use the shorter terms causes as shorthand for Granger causes. You should notice, however, that Granger causality is not causality in a deep sense of the word. It just talk about linear prediction, and it only has “teeth” if we only find Granger causality in one direction.

The definition of Granger causality did not mention anything about possible instantaneous correlation between variables. If the innovations are correlated we will say that there exits instantaneous causality

It’s possible to test Granger causality through Wald or F-test. In the

varspackage:It uses F-test to test Granger causality

Wald test for instantaneous Granger causality (non zero correlation among the \(v_{it}\))

#-- We can test Granger causality

causality(our_var, cause = c("dx")) #-- dx Granger-cause the other(s) variables?$Granger

Granger causality H0: dx do not Granger-cause dn

data: VAR object our_var

F-Test = 4.6524, df1 = 4, df2 = 348, p-value = 0.001138

$Instant

H0: No instantaneous causality between: dx and dn

data: VAR object our_var

Chi-squared = 3.5873, df = 1, p-value = 0.05822$Granger

Granger causality H0: dn do not Granger-cause dx

data: VAR object our_var

F-Test = 5.407, df1 = 4, df2 = 348, p-value = 0.0003106

$Instant

H0: No instantaneous causality between: dn and dx

data: VAR object our_var

Chi-squared = 3.5873, df = 1, p-value = 0.05822Forecasting

- We are not going to develop this topic, but… a VAR could also be used for forecasting

$dx

fcst lower upper CI

[1,] 0.3691718 -0.9506215 1.688965 1.319793

[2,] 0.1583605 -1.1744143 1.491135 1.332775

[3,] 0.2929821 -1.1194967 1.705461 1.412479

$dn

fcst lower upper CI

[1,] 0.8210940 -0.4841807 2.126369 1.305275

[2,] 0.5611573 -1.0605790 2.182894 1.621736

[3,] 0.5069927 -1.1949360 2.208921 1.701929

4. VMA represesentation

A stationary (stable) VAR could be transformed (inverted) in an infinite MA(\(\infty\)) process

By inverting the autoregressive polynomial A(L) we can obtain the VMA form of a VAR like:

\[y_{t}~=C_{0}v_{t}+C_{1}v_{t-1}+C_{2}v_{t-2}+\ ...\ [3]\]

Being \(C_{0}=I_{K}\), the rest of the \(C_{s}\) matrices could be computed recursively

- As with the VAR, model \([3]\) can be written using a polynomial in the lag operator as:

\[y_{t}=C(L)v_{t}\ \ \ \ \ \ \ \ \ \ \ \ [4]\]

being \(C(L)=(I_{K}+C_{1}L^{1}+C_{2}L^{2}+\ \ ...)\).

- Model \([3]\) or \([4]\) are also called the Wold VMA representation

Obtaining the VMA with R

First, test’s do it by hand (but with a little help from R).

- we could obtain the \(A_{i}\) matrices of the estimated VAR with the

Acoef()function

#--- Using the vars package to estimate the VAR

our_var <- VAR(variables, p = 4, type = "const") #-- estimation of the VAR

AA <- Acoef(our_var) #-- saving the A matrices in AA

AA1 <- AA[[1]] #-- AA1

AA2 <- AA[[2]] #-- AA2

AA3 <- AA[[3]] #-- AA3

AA4 <- AA[[4]] #-- AA3- To obtain the Wold VMA representation of the VAR we have to invert the \(A(L)\) polynomial. We will do it by hand and also by using the

varspackage

2a) By hand: we could obtain the VMA matrices, the \(C_{i}\), with R with the Psi() function; but by hand it would be as:

\(C_{0}=I_{K}\),

the rest of the \(C_{s}\) matrices could be computed recursively as

\[C_{s}=\underset{j=1}{\overset{s}{\sum }}C_{s-j}A_{j}\]

#-------------------------obtaining the C(i) matrices of the VMA representation

CC0 <- diag(2) #-- C(O) is the identity matrix (2x2)

CC1 <- CC0 %*% AA1

CC2 <- CC1 %*% AA1 + CC0 %*% AA2

CC3 <- CC2 %*% AA1 + CC1 %*% AA2 + CC0 %*% AA3

CC4 <- CC3 %*% AA1 + CC2 %*% AA2 + CC1 %*% AA3 + CC0 %*% AA4

CC5 <- CC4 %*% AA1 + CC3 %*% AA2 + CC2 %*% AA3 + CC1 %*% AA4 + CC0

2b) Using the vars package: we have to use the Phi() function

#--- Wold VMA of our_var with the vars package

Phi(our_var, nstep = 3) #- shows the WOLD VMA estimated matrices. (by inverting the A's matrices), , 1

[,1] [,2]

[1,] 1 0

[2,] 0 1

, , 2

[,1] [,2]

[1,] -0.09639832 -0.1181884

[2,] 0.30492251 0.7148050

, , 3

[,1] [,2]

[1,] 0.1483909 -0.3049207

[2,] 0.2427883 0.3467704

, , 4

[,1] [,2]

[1,] -0.09808845 -0.08348028

[2,] 0.19891831 0.15758298Let’s check if our calculation by hand coincide with the one obtained using the vars package. Our (by hand) CC2 matrix is:

dx.l1 dn.l1

[1,] 0.1483909 -0.3049207

[2,] 0.2427883 0.3467704

5. Uses of VAR: “Structural” analysis

The two principal instruments of VAR’s, IRF & FEVD, are defined in terms of their VMA representation [3]

IRF & FEVD will show the effects of a shock, BUT in order to have a clear meaning, they must be interpreted under the assumption that all the other shocks are held constant; however, in the Wold representation the shocks are not orthogonal; that’s why we will turn our attention to the Structural VAR models

IRFs

Usually the main interest in VAR modelling is to look at the dynamic effect of a shock on the variables of interest

This dynamic effect could be easily obtained through the VMA representation [3] of the VAR

In particular the response of the variable \(y_{n}\) to an impulse of size one in \(v_{m}\) \(j\)-periods ahead is given by the \((n,m)\)-th element of \(C_{j}\). That is, the matrices \(C_{i}\) contain the responses of the variables to the innovations for different periods (or steps) ahead

BUT…

- BUT, usually the VAR disturbances (or innovations) are correlated, then the interpretability of the impulse responses to innovation becomes problematic: if the innovations are correlated (off diagonal elements of \(\Sigma _{v}\) different from zero) then, an impulse in \(v_{m}\) would be associated with impulses in innovations at the other equations of the VAR model.

Sims proposal: Cholesky decomposition

- Therefore, Sims proposed to assume recursive contemporaneous interactions among variables, i.e. imposing a certain structural ordering in the variables. In terms of the MVA representation this means that the transformed or “structural” shocks will not affect to the preceding variables instantaneously.

In practice, imposing a recursive contemporaneous order among the variables of the VAR model, is operationalised performing a Cholesky decomposition in \(\Sigma _{v}\).

The Cholesky factor, \(P\), of \(\Sigma _{v}\) is defined as the unique lower triangular matrix such that \(PP^{^{\prime }}=\Sigma _{v}\)

- With the Cholesky factor(\(P\)) we could transform the VAR in [3] as:

\[A(L)y_{t}=PP^{-1}v_{t}\]

with \(\varepsilon _{t}=P^{-1}v_{t}\), then our transformed VAR becomes

\[A(L)y_{t}=P\varepsilon _{t}\ \ \ \ \ \ \ \ \ \ \ \ [2*]\]

That is, we have written our VAR in terms of a new vector of shocks \(\varepsilon _{t}\), with identity covariance matrix (\(\Sigma _{\varepsilon }=I\))

Now, as the \(\varepsilon _{t}\) shocks are uncorrelated their IRF would have a clear interpretation

Obtaining IRFs with R

- From [2*] we can obtain the VMA representation in terms of the \(\varepsilon _{t}\) shocks:

\[y_{t}=C(L)P\varepsilon _{t}\ \ \ \ \ \ \ \ \ \ \ \ [5\ast ]\]

\[y_{t}=D(L)\varepsilon _{t}\ \ \ \ \ \ \ \ \ \ \ \ [5]\]

being \(D(L)=C(L)P\) ,

\(D(L)=(D_{0}+D_{1}L^{1}+D_{2}L^{2}+D_{3}L^{3}-\ \ ...)\), with \(D_{i}=C_{i}P\) ,

then \(D_{0}=C_{0}P=I_{N}P=P\)

As \(D_{0}=P\), and P is lower triangular, the system is recursive: the first shock (\(\varepsilon _{t}^{1}\)) could have an instantaneous effect on all the variables of the VAR, while the first variable in the VAR could only be affected contemporaneously by \(\varepsilon _{t}^{1}\)

The matrices \(D_{i}\) contains the response of the variables to the \(\varepsilon _{t}\)

In particular the response of the variable \(y_{n}\) to an impulse of size one in \(\varepsilon_{m}\) \(j\)-periods ahead is given by the \((n,m)\)-th element of \(D_{j}\).

Don’t worry too much now because firstly we will usually do this with R and secondly because we are going to practice the calculations by hand at the Lab, but ….

- To obtain the orthogonalised IRF (the \(D_{i}\) matrices), the matrices with the IRFs

- First we have to obtain the Cholesky factor P as \(PP^{^{\prime }}=\Sigma _{v}\)

- Latter, we have to calculate the \(D_{i}=C_{i}P\) matrices

3a) By hand

VVu <- summary(our_var)[[3]] #-- The variance-covariance matrix of the residuals

PP_chol <- t(chol(VVu)) #-- Cholesky factor (matrix P in our terminology)

DD1 <- CC1 %*% PP_chol

DD2 <- CC2 %*% PP_chol

DD3 <- CC3 %*% PP_chol3b) We have to use the Psi() function (Note that the function is Psi(), not the previous Phi() ) function

, , 1

[,1] [,2]

[1,] 0.67337627 0.0000000

[2,] -0.09417032 0.6592771

, , 2

[,1] [,2]

[1,] -0.0537825 -0.07791893

[2,] 0.1380142 0.47125458

, , 3

[,1] [,2]

[1,] 0.1286374 -0.2010272

[2,] 0.1308324 0.2286178

, , 4

[,1] [,2]

[1,] -0.05818907 -0.05503664

[2,] 0.11910723 0.10389086Let’s check our DD3 with the calculations made with the var package.

dx dn

[1,] -0.05818907 -0.05503664

[2,] 0.11910723 0.10389086- Let’s show again the (Cholesky) IRF, but in the usual form:

irf(our_var, impulse = "dx", response = c("dx", "dn"), boot = FALSE, n.ahead = 6,

ortho = TRUE, cumulative = FALSE)

Impulse response coefficients

$dx

dx dn

[1,] 0.673376268 -0.09417032

[2,] -0.053782498 0.13801416

[3,] 0.128637414 0.13083241

[4,] -0.058189069 0.11910723

[5,] 0.005719843 0.12022354

[6,] -0.036212427 0.06355445

[7,] -0.020107696 0.01886216- In fact, usually IRF’s are shown in graphical form:

FEVD

FEVD : Forecast error variance decomposition

Once we have orthogonalised IRF’s (the \(D_{i}\) matrices ), the FEVD can be easily computed. Let’s see how:

- The h-step forecast error can be represented as:

\[y_{T+h}-y_{T+h\mid T}=D_{0}\varepsilon _{T+h}+D_{1}\varepsilon_{T+h-1}+\cdots +D_{h-1}\varepsilon _{T+1}\]

As \(\Sigma _{\varepsilon }=I\), the forecast error variance of the k-th component of \(y_{T+h}\) is:

\[\sigma _{k}^{2}(h)=\overset{h-1}{\underset{j=0}{\sum }}(d_{k1,j}^{2}+\cdots +d_{kK,j}^{2})=\overset{K}{\underset{j=1}{\sum }}(d_{kj,0}^{2}+\cdots +d_{kj,h-1}^{2})\]

where \(d_{nm,j}\) denotes the \((n,m)-th\) element of \(D_{j}\).

The quantity \((d_{kj,0}^{2}+\cdots +d_{kj,h-1}^{2})/\sigma _{k}^{2}(h)\) represents the contribution of the \(j\)-th shock to the h-step forecast error variance of variable \(k\).

Don’t worry too much now because firstly we will usually do this with R and secondly because we are going to practice the calculations by hand at the Lab, but ….

The FEVD are obtained through the IRF. Let’s see the FEVD and we will calculate it latter by hand:

$dx

dx dn

[1,] 1.0000000 0.00000000

[2,] 0.9868699 0.01313012

[3,] 0.9104987 0.08950130

[4,] 0.9058296 0.09417038

[5,] 0.9007024 0.09929755

[6,] 0.9006125 0.09938748

$dn

dx dn

[1,] 0.01999496 0.9800050

[2,] 0.04077447 0.9592255

[3,] 0.05972348 0.9402765

[4,] 0.07601943 0.9239806

[5,] 0.09275743 0.9072426

[6,] 0.09603517 0.9039648

Looking at the relation among IRF and FEVD

- To obtain the IRF’s we have to use the

irf()function

irf(our_var, impulse = c("dx", "dn"), response = "dx", boot = FALSE, n.ahead = 3,

ortho = TRUE, cumulative = FALSE)

Impulse response coefficients

$dx

dx

[1,] 0.67337627

[2,] -0.05378250

[3,] 0.12863741

[4,] -0.05818907

$dn

dx

[1,] 0.00000000

[2,] -0.07791893

[3,] -0.20102724

[4,] -0.05503664- To obtain the FEVD we have to use the

fevd()function

fevd() function to calculate the FEVD

$dx

dx dn

[1,] 1.0000000 0.00000000

[2,] 0.9868699 0.01313012

[3,] 0.9104987 0.08950130

[4,] 0.9058296 0.09417038

$dn

dx dn

[1,] 0.01999496 0.9800050

[2,] 0.04077447 0.9592255

[3,] 0.05972348 0.9402765

[4,] 0.07601943 0.9239806- To illustrate how to obtain the FEVD by hand, let’s first look inside the object our_irfs who will contain the IRF’s of our_var:

our_irfs <- irf(our_var, n.ahead = 5) #-- our_irfs will contain all the information about IRF

# str(our_irfs) #--- looking inside the object 'our_irfs'

class(our_irfs)[1] "varirf"With

class(our_irfs)we have seen thatour_irfsis an object of class “varirf”. Pfaff defined this type of object to allocate space to save the IRF’sOK,

our_irfsis an object of class “varirf, but withstr(our_irfs)we can look at the internal structure of the object”our_irfs" and we can see that in fact is a list of 13 elements. Too many for our purposes, then let’s concentrate only in the first element that contains the true IRF.Let’s save the first element of our_irfs to look inside again

List of 2

$ dx: num [1:6, 1:2] 0.67338 -0.05378 0.12864 -0.05819 0.00572 ...

..- attr(*, "dimnames")=List of 2

.. ..$ : NULL

.. ..$ : chr [1:2] "dx" "dn"

$ dn: num [1:6, 1:2] 0 -0.0779 -0.201 -0.055 -0.0547 ...

..- attr(*, "dimnames")=List of 2

.. ..$ : NULL

.. ..$ : chr [1:2] "dx" "dn"we can see that

our_IRF1is a list with 2 elements. The first oneour_IRF1[[1]]contains the responses of the first variable to the two shocks. The secondour_IRF1[[2]contains the responses of the second variable to the two shocksLet’s concentrate only on the movement (or responses) of the first variable (dx). The FEVD of the first variable is calculated as:

dx_e1 <- our_IRF1[[1]][, 1] #-- effect of the 1st shock in the first variable (dx)

dx_e2 <- our_IRF1[[2]][, 1] #-- effect of the 2nd shock in the first variable (dx)

d2x_e1 <- dx_e1^2 #-- IRF to the square (why?)

d2x_e2 <- dx_e2^2 #-- IRF to the square

ac_d2x_e1 <- cumsum(d2x_e1) #-- accumulating the squared IRF (why?)

ac_d2x_e2 <- cumsum(d2x_e2) #-- accumulating the squared IRF

fevd_dx_e1 = ac_d2x_e1/(ac_d2x_e1 + ac_d2x_e2) #-- % of the FEV explained by the 1st shock

fevd_dx_e2 = ac_d2x_e2/(ac_d2x_e1 + ac_d2x_e2) #-- % of the FEV explained by the 2nd shock- Let’s see, step by step, what we have done:

[1] 0.673376268 -0.053782498 0.128637414 -0.058189069 0.005719843[1] 0.00000000 -0.07791893 -0.20102724 -0.05503664 -0.05474057[1] 0.000000000 0.006071360 0.040411950 0.003029032 0.002996530[1] 0.00000000 0.00607136 0.04648331 0.04951234 0.05250887

- Checking if we have calculated the FEVD correctly:

[1] 1.0000000 0.9868699 0.9104987 0.9058296[1] 0.00000000 0.01313012 0.08950130 0.09417038$dx

dx dn

[1,] 1.0000000 0.00000000

[2,] 0.9868699 0.01313012

[3,] 0.9104987 0.08950130

[4,] 0.9058296 0.09417038

$dn

dx dn

[1,] 0.01999496 0.9800050

[2,] 0.04077447 0.9592255

[3,] 0.05972348 0.9402765

[4,] 0.07601943 0.9239806- OK, we know already how to estimate-validate-use a VAR in reduced form & to obtain and interpret the Cholesky IRF & FEDV.

- In the next Lab we will illustrate other ways to identify a SVAR